AI Search Visibility: Australian General Insurance Brands - May 2026 Report

- Arun Prasad

- 1 day ago

- 9 min read

We Tracked 20 Insurance Brands Across 34,278 Conversations. Here's Who AI Search Actually Recommends.

Your brand might rank on Google. But does ChatGPT even know you exist?

We monitored 20 Australian insurance brands across 34,278 real consumer conversations on both Google AI Overviews and ChatGPT in May 2026.

The goal: find out which brands show up when people ask AI for insurance advice.

Allianz leads with 13,437 total mentions. NRMA is right behind at 12,524. Budget Direct rounds out the top three with 10,708, and that is the May headline: Budget Direct has climbed into the top three on total AI visibility.

Then comes the drop. Brands like GIO (2,758), Shannons (2,049) and CGU (1,019) sit well below half the visibility of the leaders. And at the bottom, real brands with real customers are close to invisible in AI search: Ozicare has 62 total mentions, Coles Insurance 517, Qantas Insurance 895.

And the platforms do not agree. Budget Direct leads on Google AI Overviews (8,556 mentions) while Allianz leads on ChatGPT (5,461). Budget Direct gets four times more mentions on Google than on ChatGPT. The gap between Google visibility and AI visibility is not small. It is structural.

Brand | Google AI Overview | ChatGPT | Total |

Allianz | 7,976 | 5,461 | 13,437 |

NRMA | 7,188 | 5,336 | 12,524 |

Budget Direct | 8,556 | 2,152 | 10,708 |

AAMI | 6,156 | 3,575 | 9,731 |

RACV | 3,766 | 2,612 | 6,378 |

QBE | 4,428 | 1,630 | 6,058 |

RACQ | 4,189 | 1,536 | 5,725 |

YouI | 3,250 | 2,124 | 5,374 |

Suncorp | 3,533 | 1,593 | 5,126 |

GIO | 2,099 | 659 | 2,758 |

Shannons | 1,554 | 495 | 2,049 |

Bingle | 703 | 592 | 1,295 |

ING | 1,062 | 201 | 1,263 |

CGU | 554 | 465 | 1,019 |

Qantas | 811 | 84 | 895 |

APIA | 496 | 93 | 589 |

Coles | 457 | 60 | 517 |

Ozicare | 57 | 5 | 62 |

RAC | 5 | 36 | 41 |

RAA | 7 | 5 | 12 |

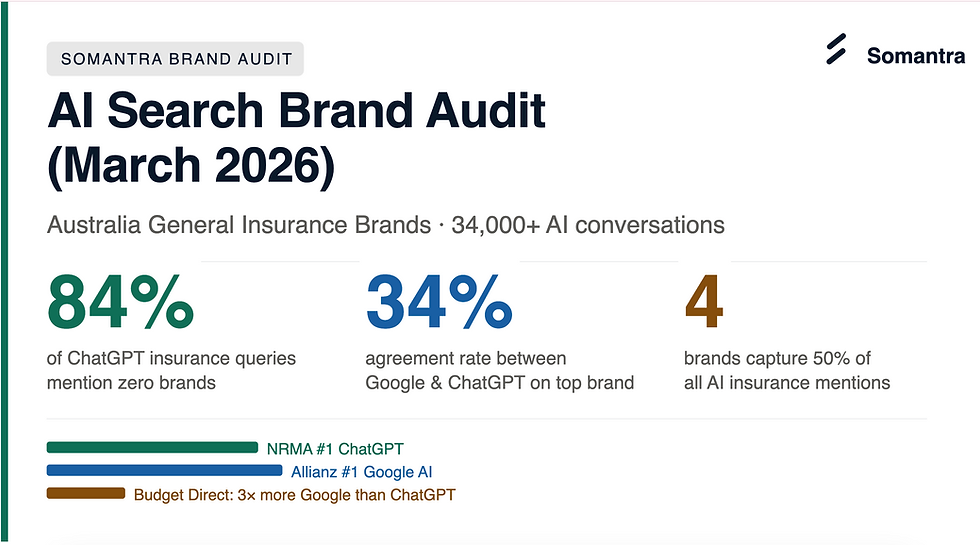

The Biggest Changes: March to May 2026

We ran the same audit in March. 2 months later, the board has moved. Here is what changed.

1. There is a new number one. In May, Allianz overtook NRMA (Leader in Mar’26) taking the top spot with 13,437 mentions (+7.7%), while NRMA stayed flat at 12,524. This proves that a brand cannot take it’s pole position for granted on AI Search.

2. Budget Direct in May showed the most improvement over it’s March performance. Up +9.7% to 10,708 mentions, climbing from #4 to #3 overall and becoming the most visible brand on Google AI Overviews (8,556 mentions, up from 7,434 in March). The caution: its ChatGPT share slipped from 23.9% to 20.1%, so the Google dependence deepened.

3. AAMI and smaller brands are losing visibility. AAMI is down -18.1% (from 11,878 to 9,731), sliding from #3 to #4. Among smaller brands the slide is steeper: Bingle -30.8%, GIO -29.3%, CGU -27.8%.

4. ChatGPT started citing, a lot more. In March, ChatGPT's most-cited source was Canstar with just 232 citations. In May, Finder (902) and Canstar (901) both cleared 900, roughly four times March's volume, and Finder took the #1 spot. Reddit grew from 147 to 387 citations.

5. The AI source pool is consolidating. The engines cited 10,777 unique domains in March but only 8,488 in May, a 21% contraction in who gets a voice. Fewer sources means it requires higher stakes for being one of them. We anticipate that both publisher and brand sites will now focus on building “trust authority” to be cited.

6. Brands are surfacing more often in deep conversations. Zero-brand Conversation answers fell from 84.1% to 82.4% on ChatGPT and from 60.6% to 55.5% on Google.In our March report we had pointed this out as an opportunity and now we see brands taking advantage of the whitespace. The window is closing: every month, more of the long tail gets claimed.

7. The engines disagree most of the time. Top-brand agreement between Google and ChatGPT rose from 23.7% in March to 27.9% in May. Even so, in roughly seven of ten head-to-head queries the two engines still recommend different brands.

Brand | March'26 total mentions | May'26 total mentions | Absolute change | % change |

Budget Direct | 9,765 | 10,708 | 943 | 9.66% |

Allianz | 12,477 | 13,437 | 960 | 7.69% |

QBE | 5,853 | 6,058 | 205 | 3.50% |

NRMA | 12,522 | 12,524 | 2 | 0.02% |

Youi | 5,407 | 5,374 | -33 | -0.61% |

ING | 1,286 | 1,263 | -23 | -1.79% |

RACQ | 6,017 | 5,725 | -292 | -4.85% |

RACV | 6,779 | 6,378 | -401 | -5.92% |

Suncorp | 5,852 | 5,126 | -726 | -12.41% |

Shannons | 2,447 | 2,049 | -398 | -16.26% |

AAMI | 11,878 | 9,731 | -2147 | -18.08% |

CGU | 1,412 | 1,019 | -393 | -27.83% |

GIO | 3899 | 2,758 | -1141 | -29.26% |

Bingle | 1,871 | 1,295 | -576 | -30.79% |

Myth: Google AI Overview Visibility Translates into ChatGPT Visibility

Out of 20 Australian insurance brands we track, several are effectively invisible on ChatGPT. Qantas Insurance gets just 9.4% of its total visibility from ChatGPT. Coles Insurance gets just 11.6% of its total visibility from ChatGPT. APIA gets just 15.8% of its total visibility from ChatGPT.

These brands show up on Google. They have websites, they run ads. But when a consumer asks ChatGPT "what is the best car insurance in Australia", they do not get mentioned.

On the other end, Bingle is the healthiest brand on ChatGPT: 46% of its total visibility comes from it. CGU (46%) and NRMA (43%) also hold a real presence on both platforms.

Budget Direct is the most dramatic divergence story in the market. It is the most visible brand on Google AI Overviews, yet only 20.1% of its visibility comes from ChatGPT. For every five times Budget Direct appears across both platforms, four are on Google and one is on ChatGPT.

If your brand is strong on Google but weak on ChatGPT, you have a visibility gap that is only going to widen. The fix is not more SEO. It is a fundamentally different content strategy.

Brand | Google AI Overviews | ChatGPT | Total | ChatGPT share % |

Budget Direct | 8,556 | 2,152 | 10,708 | 20.1% |

Allianz | 7,976 | 5,461 | 13,437 | 40.6% |

NRMA | 7,188 | 5,336 | 12,524 | 42.6% |

AAMI | 6,156 | 3,575 | 9,731 | 36.7% |

QBE | 4428 | 1630 | 6,058 | 26.9% |

RACQ | 4,189 | 1,536 | 5,725 | 26.8% |

RACV | 3,766 | 2,612 | 6,378 | 41% |

Suncorp | 3,533 | 1,593 | 5,126 | 31.1% |

Youi | 3,250 | 2,124 | 5,374 | 39.5% |

GIO | 2,099 | 659 | 2,758 | 23.9% |

Shannons | 1,554 | 495 | 2,049 | 24.2% |

ING | 1,062 | 201 | 1,263 | 15.9% |

Qantas Insurance | 811 | 84 | 895 | 9.4% |

Bingle | 703 | 592 | 1,295 | 45.7% |

CGU | 554 | 465 | 1,019 | 45.6% |

APIA | 496 | 93 | 589 | 15.8% |

Coles Insurance | 457 | 60 | 517 | 11.6% |

Ozicare | 57 | 5 | 62 | 8.1% |

RAA Insurance | 7 | 5 | 12 | 41.7% |

RAC Insurance | 5 | 36 | 41 | 87.8% |

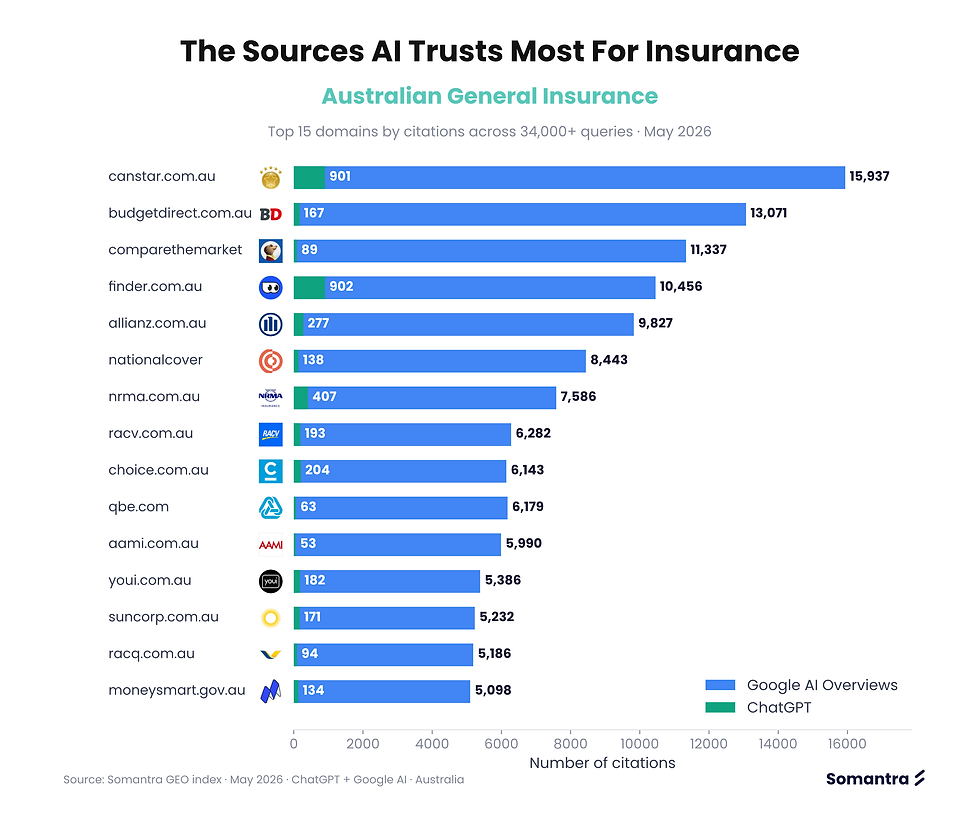

Trust Authority : Most Cited Sites

SEO has always been about earning trust from Google. But there is a new gatekeeper, and it does not care about your backlink profile.

Canstar is the single most cited domain: 16,838 total citations across both platforms, 15,937 of them on Google AI Overviews. It is the undisputed king of traditional search authority for insurance content.

But ChatGPT tells a different story. Finder (902 citations) and Canstar (901) are both equally trusted by ChatGPT as a source. The surprise is third place among third parties: Reddit, with 387 citations, a forum, not a comparison site. Forbes comes in at 256 and moneysmart.gov.au, the government's financial literacy site, at 134.

The comparison-site effect is real but smaller than you might expect: Canstar, Compare the Market, Finder, iSelect, Choice and friends account for 16.1% of all citations. Brand-owned sites make up 26.5%, and the rest comes from third-party editorial, media, government and community sources.

Here is the insight that matters. If you want ChatGPT to recommend your brand, being on your own website is not enough. You need to be mentioned positively on the sites AI trusts. This is not link building. It is reputation building across the sources that train and inform AI models.

Domain | Google citations | ChatGPT citations | Total citations |

15,937 | 901 | 16,838 | |

13,071 | 167 | 13,238 | |

11,337 | 89 | 11,426 | |

10,456 | 902 | 11,358 | |

9,827 | 277 | 10,104 | |

8,443 | 138 | 8,581 | |

7,586 | 407 | 7,993 | |

6,282 | 193 | 6,475 | |

6,143 | 204 | 6,347 | |

6,179 | 63 | 6,242 | |

5,990 | 53 | 6,043 | |

5,386 | 182 | 5,568 | |

5,232 | 171 | 5,403 | |

5,186 | 94 | 5,280 | |

5,098 | 134 | 5,232 |

Car Insurance vs Pet Insurance: Where AI Sends You Is Very Different.

Not all insurance product lines are created equal, at least not in the eyes of AI.

The competetive product categories:

Car insurance dominates with 22,777 total brand mentions across ChatGPT and Google.

Home & contents follows at 20,591.

Motorcycle comes third at 16,376.

These are crowded, competitive spaces where the big brands fight hard for visibility.

Pet insurance sits near the bottom with just 2,457 mentions and life insurance is even lower at 1,283. These product lines are underserved, with fewer brands competing and far more room for one brand to own the conversation.

Brand concentration varies wildly by product line too. NRMA leads car insurance with 3,238 mentions. QBE leads motorcycle with 2,896. Allianz owns travel (3,941), and Budget Direct owns pet (940).

Source diversity paints an even sharper picture. When someone asks about car insurance, Google pulls from 2,101 unique domains; ChatGPT uses 481. For home insurance it is 2,600 vs 355. Fewer sources means fewer brands get a voice.

And the comparison-site effect differs by product line: pet insurance leans hardest on aggregators (19.9% of citations) while roadside assistance is the most direct, brand-to-consumer conversation (5.2%).

Some product lines are a trench battle. Others are an open field. Know which one you are in before you plan your next content push.

Brand | Car | Home & Contents | Motorcycle | Roadside | Other | Travel | Pet | Life | Row total |

Allianz | 2,762 | 3,447 | 928 | 800 | 1,518 | 3,941 | 143 | 308 | 13,847 |

NRMA | 3,238 | 3,731 | 2,536 | 1,086 | 1,061 | 732 | 25 | 49 | 12,458 |

Budget Direct | 3,185 | 2,738 | 1,413 | 488 | 766 | 857 | 640 | 192 | 10,279 |

AAMI | 2,600 | 2,799 | 1,361 | 520 | 906 | 56 | 555 | 243 | 9,040 |

RACV | 1,846 | 928 | 1,207 | 1,708 | 494 | 375 | 26 | 16 | 6,600 |

QBE | 691 | 1,572 | 2,896 | 18 | 548 | 253 | 7 | 51 | 6,036 |

RACQ | 1,462 | 962 | 996 | 1,843 | 315 | 300 | 387 | 21 | 6,286 |

Youi | 1,498 | 1,252 | 1,648 | 184 | 500 | 21 | 242 | 37 | 5,382 |

Suncorp | 1,670 | 1,360 | 713 | 76 | 443 | 42 | 55 | 283 | 4,642 |

GIO | 1,050 | 952 | 344 | 91 | 231 | 4 | 21 | 11 | 2,704 |

Shannons | 284 | 1,678 | 45 | 16 | 1 | 2,024 | |||

Bingle | 988 | 142 | 88 | 24 | 49 | 3 | 1,294 | ||

ING | 678 | 313 | 428 | 10 | 1 | 25 | 8 | 1,463 | |

CGU | 144 | 424 | 220 | 4 | 183 | 3 | 14 | 20 | 1,012 |

Qantas Insurance | 312 | 398 | 3 | 34 | 146 | 893 | |||

APIA | 193 | 260 | 71 | 9 | 17 | 1 | 5 | 30 | 586 |

Coles Insurance | 252 | 226 | 4 | 5 | 17 | 2 | 8 | 1 | 515 |

Ozicare | 2 | 60 | 62 | ||||||

RAC Insurance | 13 | 5 | 5 | 5 | 6 | 2 | 1 | 37 | |

RAA Insurance | 1 | 3 | 1 | 1 | 6 | 12 |

Is AI Creating Brand Monopolies in Insurance? The Data Says Yes.

Google gives you options. ChatGPT gives you a shortlist, and the shortlist is getting shorter.

On ChatGPT, just 3 brands account for 50% of all insurance mentions. 5 brands control 60%, 7 control 75% and 9 control 90%. If you are not in the top tier, you are fighting over scraps of visibility.

Google AI Overviews is more democratic, but not by much: 4 brands make up 50% of mentions, 5 reach 60%, 8 reach 75% and 11 cover 90%. The long tail is longer; more brands get a seat at the table.

And the two platforms still mostly disagree. Across 4,380 queries where both platforms named brands, Google and ChatGPT agreed on the top brand only 27.9% of the time, up from 23.7% in March, the two biggest answer engines in the world still told consumers different things about insurance in roughly 72% of head-to-head queries.

70% of long tail insurance questions on AI Search mention Zero Brands. That Is Whitespace Opportunity.

We tracked 34,278 conversation queries and found that the long-tail, specific questions where real consumers actually require guidance e.g. "how to claim pet insurance for overseas pets" and "what car insurance discounts are available for new cars", 70% of those queries returned zero brand mentions.

This is not a problem. This is an opportunity. Every one of those brandless GoogleAI Overview or ChatGPT response is a gap in the market, proving a place where the right content, structured the right way, published on the right sources, could put your brand into the AI's answer.

First mover advantage in AI search is real. And right now, most of the field is wide open.

Google and ChatGPT don't recommend the same brand for a query most of the time. Here's What That Means.

When users ask Google AI Overviews and ChatGPT the same insurance question. You will get different answers most of the time. The best performaing brands like Allianz, NRMA achieve consistent recommendation for a query across both Google AI Overview and ChatGPT only in the 20%-25% range.

This is a challenge and an opportunity. For large brands who have spent the last decade spending time on dominating a single search platform , they now face a landscape where consumers expect brand presence on multiple search engines ; brands are required to create a consistent message across all the AI search engines. A typical insurance consumer is researching on both Google AI Overview and ChatGPT.

This expands the surface area for brands to present themselves in the consumers buying journey there by increasing the opportunity to grow brand mindshare.

The dual combination of expanded opportunity surface area coupled with divergence in brand recommendations from the different AI Search engines is the biggest opportunity for brands.

Brand | Agreed queries (brand mentioned in AI response on both engines) | Not-agreed queries | Only Google | Only ChatGPT | Total queries | Agreed % |

Allianz | 1884 | 5622 | 3397 | 2225 | 7506 | 25.1% |

NRMA | 1446 | 5360 | 3215 | 2145 | 6806 | 21.2% |

Budget Direct | 799 | 5568 | 4839 | 729 | 6367 | 12.5% |

AAMI | 923 | 4761 | 3096 | 1665 | 5684 | 16.2% |

RACV | 476 | 3317 | 2118 | 1199 | 3793 | 12.5% |

QBE | 483 | 2841 | 2057 | 784 | 3324 | 14.5% |

RACQ | 472 | 2707 | 2145 | 562 | 3179 | 14.8% |

Suncorp | 255 | 2914 | 2108 | 806 | 3169 | 8.0% |

Youi | 474 | 2556 | 1579 | 977 | 3030 | 15.6% |

GIO | 91 | 1857 | 1478 | 379 | 1948 | 4.7% |

Shannons | 152 | 869 | 679 | 190 | 1021 | 14.9% |

ING | 38 | 713 | 621 | 92 | 751 | 5.1% |

CGU | 41 | 704 | 381 | 323 | 745 | 5.5% |

Qantas Insurance | 18 | 726 | 670 | 56 | 744 | 2.4% |

Bingle | 72 | 628 | 295 | 333 | 700 | 10.3% |

Coles Insurance | 11 | 416 | 379 | 37 | 427 | 2.6% |

APIA | 4 | 378 | 320 | 58 | 382 | 1.0% |

Ozicare | 0 | 50 | 46 | 4 | 50 | 0% |

RAC Insurance | 0 | 40 | 5 | 35 | 40 | 0% |

RAA Insurance | 0 | 11 | 7 | 4 | 11 | 0% |

Comments